Economic impacts of a health care plan to cover all Maine residents

In 2018, Maine AllCare contracted with the Maine Center for Economic Policy (MECEP) to conduct a study of the costs and economic impacts of a health care model that would cover all Maine residents through a state-level public plan, with no fee at the point of service. The results of the study show that total yearly health care spending could decrease by $1.5 billion under a new public plan, delivering significant benefits to Maine residents, cities, towns and employers, along with fiscal stability for health care providers and hospitals.

How would a new public plan work?

MECEP based their model on the following assumptions:

- The new plan would be the primary source of coverage for those who currently have employer-based and individual coverage. It would cover the uninsured, and fill coverage gaps for those on Medicare, MaineCare, VA, TRICARE and Indian Health.

- The new plan would provide all the benefits of Medicare or Medicaid and add dental, vision and hearing benefits.

- The new plan would have no co-pays, coinsurance or deductibles.

- The new plan would reimburse providers and hospitals at current Medicare rates.

Impacts of a new public plan

For Maine families and individuals:

Under a plan to cover everyone in Maine, 80% of families and individuals would see a boost in household income due to savings on insurance and out-of-pocket health costs. With lower spending on health care, Maine families would have more disposable income. Maine citizens would have medical, vision, hearing and dental coverage. In addition, increased access to primary care and prevention would promote early diagnosis, timely treatment and improved management of illness, including expensive chronic illness, which would improve health while reducing costs.

Sliding scale premiums ensure that all Maine residents contribute based on ability to pay

- Below 138% of FPL – no premium

- 139% to 399% of FPL – 2 to 5% of AGI

- 400% to 499% of FPL – 5 to 6% of AGI

- 500% of FPL or above – 7.5% of AGI

- Families above $150,000 pay full premium

(FPL: Federal Poverty Level ($12,490) AGI: Adjusted Gross Income)

Full annual premium: $6,000 per adult; $3,500 per child; $3,000 for 65+

For Maine cities and towns:

Municipalities, counties and school districts would see a net savings of just over $214 million, or 8.4% of current property tax, equivalent to a property tax reduction of 1.5 mills. These savings could be used for education, town services and reduction in property taxes.

For Maine employers:

Most employers would pay the same or less they do now, with their costs based on number of employees. Employers would eliminate the costs of choosing and managing coverage plans. Workers' compensation premiums would be cut in half. Improvements in access to care and in overall health would improve employee productivity. Coverage for everyone would lead to greater flexibility for employers and for workers.

Fee structure for employers:

- Fewer than 10 employees – 3% of payroll

- 10-99 employees – 4.5% of payroll

- 100+ employees – 10% of payroll

For Maine hospitals and providers:

A public plan would pay providers and hospitals promptly and directly. The state would not own hospitals or doctors’ offices. Payments to hospitals, physicians and physicians’ groups would be made at Medicare rates. Uncompensated “charity” care would be eliminated.

Most providers would see minimal, if any, net financial effects. Reduced private insurance payments would be offset by higher Medicaid reimbursement levels; elimination of bad debt and charity care; savings on health insurance for employees; and simplified administration of billing and insurance.

Jobs and economic impacts

MECEP estimates that under a public model, 2,931 fewer administrative jobs in hospitals, doctors’ offices, and businesses would be needed, due to greatly simplifying the system. Wage replacement and retraining costs are taken into consideration in the report. Broader economic benefits would accrue from a healthier workforce, along with increased entrepreneurship when insurance is decoupled from employment.

Maine health care costs keep rising and coverage keeps shrinking

- Between 2006 and 2018, the average premium for a single employee on an individual plan increased from $4,663 to $6,866. (One-and-a-half times the increase in the cost of living over that period)

- The average annual employee contribution for an individual plan increased from $1,100 to $1,461.

- The average annual employer contribution for an individual plan increased from $3,600 to $5,403.

- The average individual deductible for an employer-sponsored plan increased from $800 to $2,447.

- The share of Maine employees eligible for a plan through their employer fell from 73% to 61%.

Health care spending was 17% of Maine’s economy in 2001, 25% in 2018 and projected to be 27% in 2026. The cost of health care is expected to reach $16,000 per person in Maine by 2026. There are 74,000 uninsured people in Maine and one in seven Mainers skipped care in 2018 because of costs, compared to one in ten in 2006.

Primary sources of insurance in Maine in 2017: Employer-based (43%); Medicare (23%); MaineCare (20%); Affordable Care Act (6%); Uninsured (5.5%); VA/Tricare/Indian Health (2.5%)

How do we pay for a new public plan?

The MECEP team estimates that the net cost for a plan to cover everyone in Maine would be just under $5 billion. This is after applying state savings as well as federal funds currently coming to the state for Medicaid reimbursement and Affordable Care Act subsidies. Approximately $4 billion would come from recapturing the funds now paid as premiums by individuals, families, and employers.

The remaining $1 billion could come from sources such as an additional income tax on individual incomes over $200,000, increases in restaurant and lodging taxes, eliminating some state tax subsidies, broadening the sales tax to include certain services that are not currently taxed, restoring the estate tax, and increasing excise taxes on tobacco and alcohol.

How much would a public plan cost?

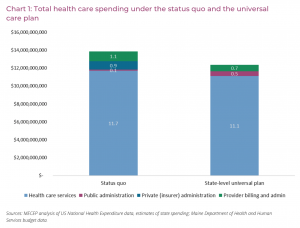

Maine spent $13.9 billion on health care in 2017. MECEP estimates that a public plan would decrease this to an equivalent of $12.4 billion. Of this decrease, $600 million would come from lower reimbursement rates and $900 million would come from net administrative savings, including the elimination of private insurance administrative costs, marketing and profit.

Conclusion

While a state-based public plan would require broad changes in the way healthcare coverage is paid for in Maine, it would lower overall spending. A state-based public plan could also provide significant benefits to Maine residents, municipalities and employers as well as bring fiscal stability to our healthcare providers and hospitals.

View the full MECEP economic feasibility study HERE.

View a 4-page summary of the MECEP study HERE.

Real examples of health care costs drawn from a survey of Maine families:

| Family Size | Income | Current costs |

% of income |

Costs under new plan |

% of income |

| 1 Parent, 2 kids | $10,000 | $1,200 | 12% | $160 | 2% |

| Family of 3 | $40,000 | $6,500 | 16% | $2,500 | 6.3% |

| Family of 3 | $75,000 | $7,100 | 9.5% | $4,050 | 5.4% |

| Family of 4 | $120,000 | $10,500 | 8.8% | $8,640 | 7.2% |

| Couple | $210,000 | $9,900 | 4.7% | $12,990 | 6.2% |

| Couple | $500,000 | $2,200 | 0.4% | $27,070 | 5.9% |

| Retired couple | $25,000(SS) | $3,200 | 12.3% | $1,250 | 4.3% |

A single mother, 38, earning $10,000 a year, with two children, ages 9 and 4:

The family currently qualifies for MaineCare, with no monthly premiums. However, it’s not uncommon for families like this to incur out-of-pocket expenses for services not covered. Perhaps the mother needs a tooth extracted, or one of the daughters needs to replace a pair of lost eyeglasses. These expenses could total $1,200 or 12% of annual income.

Under the public plan model, the range of services would be expanded to eliminate the need for additional out-of-pocket costs. Increased reimbursement rates could also increase provider options. Many low-income Mainers also suffer from unpredictability of income. Perhaps they work seasonal jobs, or jobs with varying schedules. This can make them eligible for MaineCare for a short period of time, before losing it as their income increases. A public plan model would bring increased stability to these families. Based on consumer expenditure patterns, increases to sales and excise taxes outlined in the public plan model would cost this family an additional $160 per year, for a total cost of 2% of annual income. Their net savings would be $1,040.

Lower middle class parents with one child, earning $40,000 a year from their small business:

They purchase their insurance through the Affordable Care Act’s online marketplace. Because of their relatively low income, annual premiums are capped at $2,500 per year. However their plan has a high deductible, and total out-of-pocket expenses for the year are $4,000, or 16% of annual income.

Under the public plan model, premiums are capped at 2.8% of annual income ($1,120) with no co-pays or deductibles. The additional sales tax liability would be $280, and loss of itemized deductions increases state income tax liability by $100. Their small business has two employees. The 3% payroll tax minus the reduced workman’s compensation costs $1,000 a year. They would pay 6.2% of annual income with a net savings of $2,500.

Upper-middle income family, earning $75,000, with employer insurance:

Two parents with one child are insured through a plan offered by the mother’s employer. The employer covers about three-quarters of the cost of the premiums, but the family still contributes $3,600 a year. On top of that, they incur $3,500 in out-of-pocket expenses, for a total of $7,100 or 9.5% of annual income.

Under a public plan model, the baseline premium would be $15,500 ($6,000 for each adult, plus $3,500 for the child.) But based on their income, their cost is capped at 4.7% of annual income, or $3,525 per year. The additional sales and excise tax liability would be $450; loss of itemized deductions would increase their state income taxes by $75. Costs would go down to 5.4% of annual income and the family would save $3,950 per year.

Upper income family, earning $120,000, with employer-based insurance:

The employer plan covers most of the premium cost for the parents and two children, leaving the family to pay $2,000 a year. Additionally, they incur $8,500 of out-of-pocket costs a year. Their total annual health care spending is $10,500, or 8.8% of their annual income.

Under a public plan model, their baseline cost is $19,000 ($6,000 per adult, plus $3,500 per child). Based on their income, their fee is capped at 6.0% of annual income, or $7,200 per year. Their additional annual sales tax liability would be $480. The end of itemized deductions increases their state income taxes by $960. Total cost of the public plan model for this family would be $8,640, or 7.2% of annual income. On net, the family would save $1,860 per year.

Wealthy couple, earning $210,000 a year, with individual insurance:

The couple work as professionals with their own independent businesses and purchase a plan on the individual market. They pay $3,600 a year in premiums, and incur $6,300 in out-of-pocket costs, for a total of $9,900 annually, or 4.7% of income.

Under a public plan model, the baseline premium would be $12,000 ($6,000 per adult). As a high-income family, they are liable for the full cost. Their additional annual sales tax liability would be $630. The end of itemized deductions increases their income tax liability by $360. The creation of the new income tax bracket at $200,000 does not impact this family, after adjusting for deductions. The total cost would be 6.2% of annual income and the couple would pay an additional $3,090 under the new plan.

Wealthy couple, earning $550,000:

One person runs their own business, the other works independently as a hedge fund manager. They are covered through an employer-sponsored plan, and currently pay $5,000 a year in premiums, plus an average of $7,500 out of pocket every year, for a total cost of $12,500 or 2.3% of annual income.

Under a public plan model, their base premium is $12,000 per year ($6,000 per adult). Their additional annual sales tax liability would be $5,500. The end of itemized deductions increases their income tax liability by $1,870. The creation of the new income tax brackets at $200,000 and $500,000 increases their state income tax liability by just under $9,900 a year. This couple would pay 5.3% of income, or $29,270.

The business owner currently offers health insurance to some of her 40 employees, at a total cost of $60,000 a year to the business. Under the Maine AllCare plan, her business would instead pay a 5.5% payroll tax on her employee payroll of $975,000. Her total payroll tax liability would be $53,625, a net saving of $6,375 compared to providing insurance under the status quo. Additionally, her workers’ compensation premiums would be reduced by $321 per worker per year, or $12,840. Total business savings are therefore $19,215. She could either pass these savings along to workers as higher wages, reinvest them in her business, or keep the savings as additional profit.

Senior retired couple, earning $25,000 a year from Social Security:

Both are enrolled in Medicare and they purchase a Medigap plan. Currently they pay $1,300 in premiums and $1,900 out of pocket every year, or 12.3% of annual income.

Under a public plan model, they would no longer need a Medigap plan, and out-of-pocket copayments would be eliminated. They would also have access to services like dental and hearing care, which are not covered under basic Medicare. The premium would be capped at 4.2% of their annual income, or $1,050 a year. Based on consumer expenditure patterns, the increases to sales and excise taxes outlined in the new plan would cost this family an additional $200 a year for a total cost of 4.3% of annual income. Net savings would be $1,950.